A straight-talking guide for GCs and home remodeling businesses

Look, I get it. You became a contractor to build things, not to become a salesperson pushing loans on people. But here's the reality check we all need: if you're not offering financing to your customers, you're leaving serious money on the table and losing jobs to competitors who are.

The good news? You don't have to turn into some slick-talking used car salesman to make financing work for your business. In fact, the best approach is the complete opposite. Be helpful, be honest, and make it about solving your customer's problems, not padding your wallet.

Let me break down everything you need to know about offering financing the right way, backed by real data that'll make you wonder why you haven't been doing this already.

The Numbers Don't Lie: Why Financing Is a Game-Changer For General Contractors

Before we dive into the how, let's talk about the why. The statistics around contractor financing aren't just impressive, they're eye-opening.

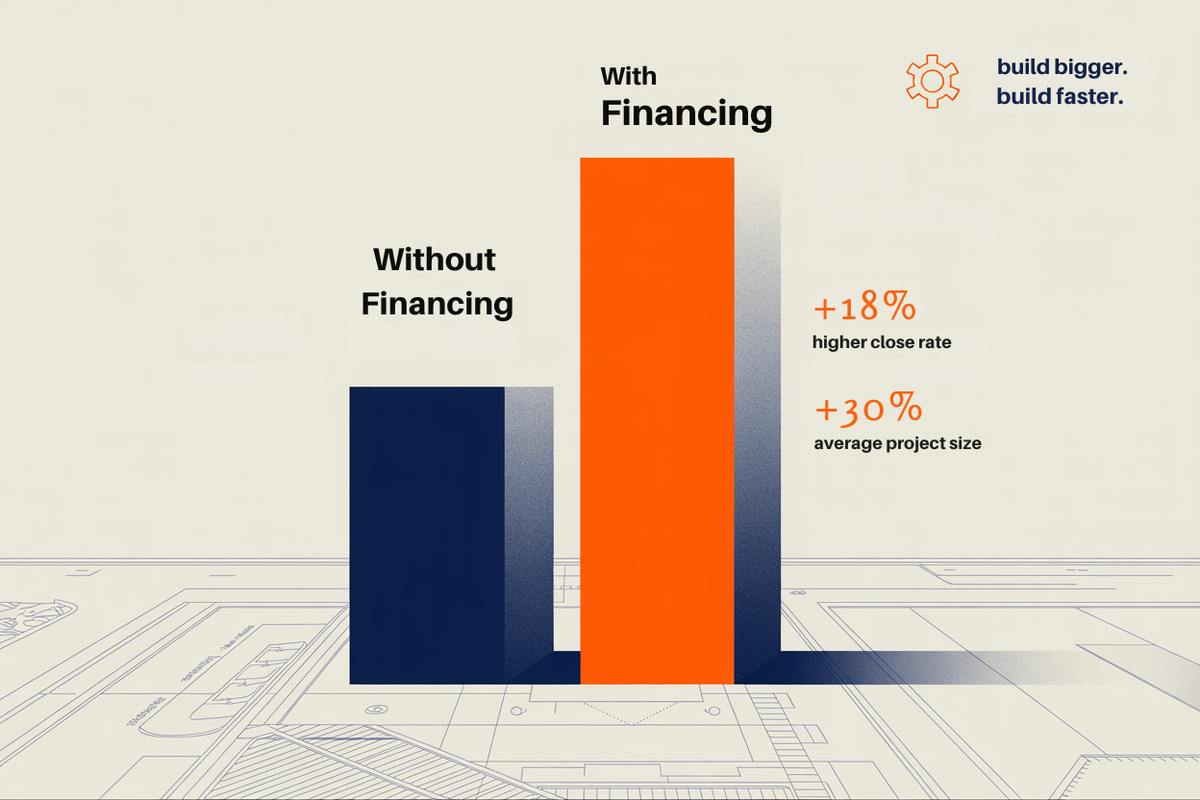

According to recent industry research, contractors who offer financing see an 18% higher close rate and 30% larger average project size. Think about that for a second. Nearly one in five more jobs closed, and each job is 30% bigger. If you're doing $500K a year, that could mean an extra $240K in revenue just by offering financing options.

But it gets better. Other studies show that offering financing can lead to 50% higher project tickets and more than a 20% increase in closing rates. Some contractors report even higher numbers, we're talking about transformational changes to your business, not just minor improvements.

Here's another stat that'll blow your mind: home improvement is now the third most common reason Americans take out personal loans. That's right, after debt consolidation and paying off credit cards, fixing up their house is the next biggest reason people borrow money. Personal loan balances hit a record $253 billion in Q1 2025, and about 7% of those borrowers, over 1.6 million people, used those funds for home improvement.

What does this tell us? Your customers are already thinking about financing. They're already comfortable with the idea of borrowing money for home improvements. The question isn't whether they want financing, it's whether you're going to be the one to offer it to them, or if they're going to go find it somewhere else (and maybe find a different contractor while they're at it).

The Reality of Customer Budgets

Let's be real about what we're dealing with out there. The average kitchen remodel costs $25,000, and a bathroom remodel runs about $10,000.. Most homeowners don't have that kind of cash just sitting around in their checking account, and even if they do, they might not want to spend it all at once.

Here's what the research tells us about homeowner behavior: Nearly 70% of homeowners plan to use financing for major projects]. Almost half, 48%, actually prefer financing over paying out-of-pocket, even when they have the cash available. Why? Because it preserves their emergency fund, helps with cash flow, and lets them tackle bigger projects than they could afford upfront.

Think about your own customers. How many times have you heard, "We love the proposal, but we need to save up for a few months"? Or "Can we do this in phases because we can't afford it all at once"? Those are financing opportunities you're missing.

When a customer says they need to "think about it" or "save up," what they're really saying is, "I want this, but I can't afford to pay for it all upfront." That's your cue to introduce financing, not as a sales pitch, but as a solution to their problem.

Why Every Contractor Should Offer Financing (Beyond Just More Sales)

Sure, the increased close rates and bigger project sizes are compelling, but the benefits of offering financing go way deeper than just more revenue. Let's talk about what financing really does for your business.

Faster Cash Flow and Better Payment Terms

When you offer financing through a third-party provider, you typically get paid upfront or in stages, just like any other job. The difference is that your customer doesn't have to come up with all the cash at once. The financing company pays you, and they handle collecting payments from the homeowner.

This is huge for cash flow. Instead of waiting for customers to save up money or doing payment plans where you're essentially the bank, you get paid on your normal schedule while the customer gets the payment terms they need.

Competitive Advantage That Actually Matters

Here's something most contractors don't think about: 78% of jobs go to the first contractor to get to the lead. But what happens when you're not the first one there? You need something to differentiate yourself, and financing is one of the most powerful differentiators you can offer.

When you can say, "We can get you approved for financing today and start work next week," while your competitor is telling them to "save up and call us in six months," who do you think gets the job?

Bigger Projects, Happier Customers

When customers aren't constrained by their available cash, they tend to say yes to more of what they actually want. That bathroom remodel that was going to be basic fixtures and a coat of paint suddenly becomes the full renovation with the tile they really wanted and the vanity that fits the space perfectly.

This isn't about upselling for the sake of upselling, it's about helping customers get what they actually want instead of settling for what they can afford upfront. And happy customers who got what they wanted are the ones who leave great reviews and refer their friends.

Reduced Project Delays and Cancellations

How many times have you had a project get delayed or cancelled because the customer's financial situation changed? Maybe they had an unexpected expense, or their bonus didn't come through, or they just got cold feet about spending so much cash.

When customers finance their projects, they're less likely to cancel or delay because their monthly payment stays the same regardless of what else happens in their financial life. It's much easier to commit to $300 a month than to commit to $15,000 all at once.

The Right Way to Introduce Financing (Without Being Pushy)

Now here's where most contractors get it wrong. They think offering financing means becoming a salesperson, pushing loans on people who don't want them. That's not just wrong, it's counterproductive.

The key to selling financing without being pushy is to make it about solving problems, not making sales. Here's how to do it right.

Start with Understanding, Not Selling

Before you ever mention financing, you need to understand what your customer is trying to accomplish and what their constraints are. Ask questions like:

- "What's your timeline for getting this project done?"

- "Are you planning to tackle this all at once, or were you thinking about doing it in phases?"

- "What's most important to you, getting everything you want, or keeping the upfront cost down?"

Listen to their answers. If they mention budget constraints, timeline concerns, or wanting to do things in phases, those are natural openings to discuss financing options.

Present It as a Solution, Not a Sales Pitch

When you introduce financing, frame it as a solution to a problem they've already told you about. Instead of saying, "We offer financing," try something like:

"You mentioned you'd like to get this done before the holidays but you're concerned about the upfront cost. We work with a financing partner that could break this into monthly payments of around $200. Would that make the timeline work better for you?"

Notice how this approach acknowledges their stated concern and offers financing as a specific solution to that concern. You're not pushing a loan, you're solving a problem.

Be Transparent About the Process

One reason people get uncomfortable with financing offers is that they don't understand how it works or they're worried about hidden costs. Be upfront about the process:

"Here's how it works: you fill out a quick application, usually takes about five minutes. If you're approved, the financing company pays us directly, and you make monthly payments to them. There's no cost to you for applying, and if you're not approved or you decide not to use it, there's no obligation."

Transparency builds trust, and trust is what turns prospects into customers.

Don't Make It About You

This is crucial: never make financing about what it does for your business. Don't say things like, "This helps us get paid faster," or "We prefer customers who finance." Keep the focus entirely on how it benefits them.

Instead of talking about your business needs, focus on their goals: "This would let you get the whole project done at once instead of having to wait and do it in phases," or "You'd be able to keep your savings intact for emergencies while still getting the kitchen you want."

Understanding Your Financing Options

Not all financing is created equal, and understanding the different options will help you choose the right approach for your business and your customers.

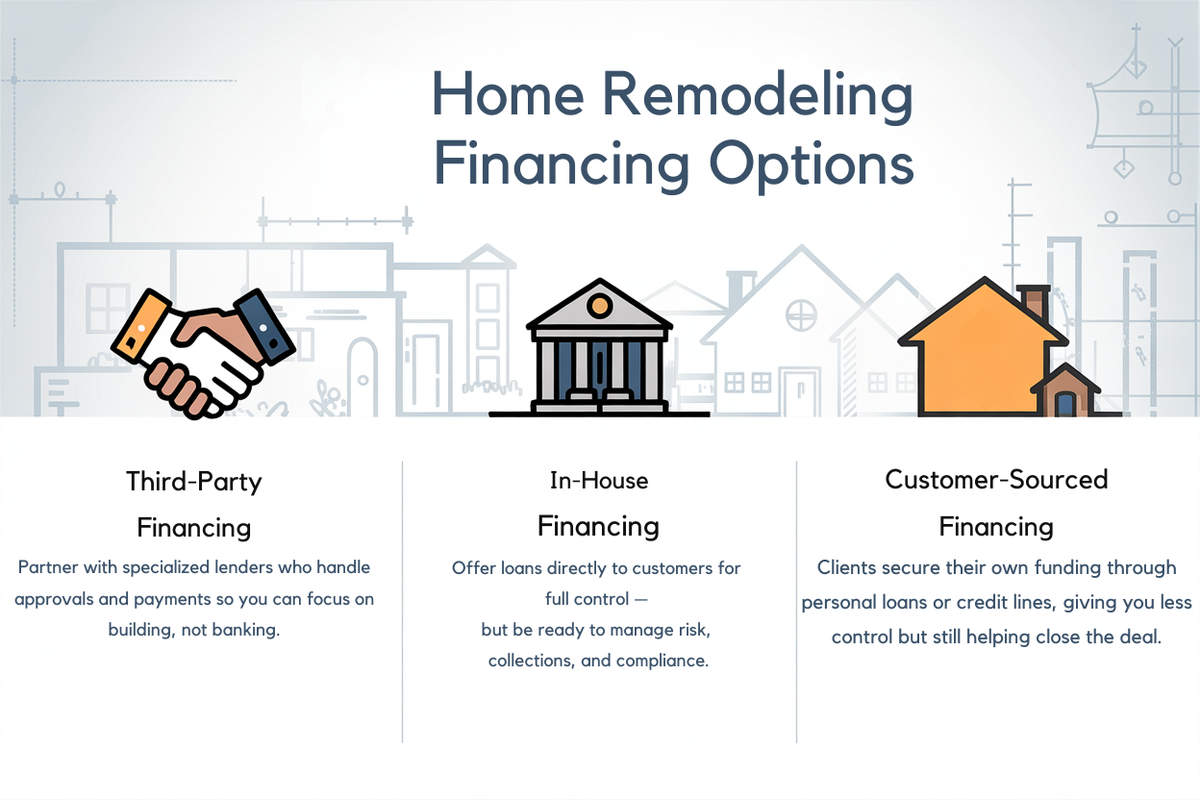

Third-Party Financing (The Smart Choice for Most Contractors)

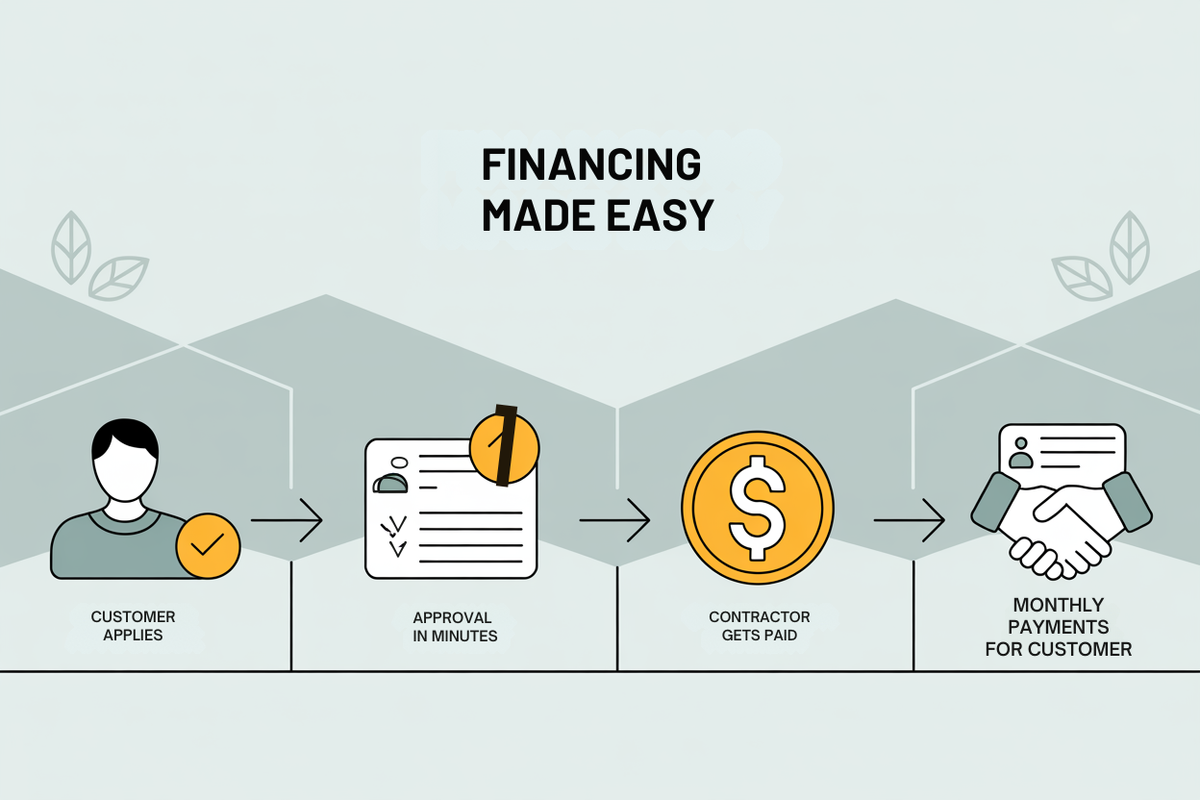

This is what most successful contractors use, and for good reason. You partner with a financing company that specializes in home improvement loans. They handle the credit checks, approvals, and loan servicing, while you get paid just like any other job.

The customer applies for financing, gets approved (hopefully), and the financing company either pays you directly or gives the customer the funds to pay you. Either way, you're out of the loan business and back in the construction business where you belong.

Popular third-party financing companies include Greensky, Hearth, Acorn Finance, and others. Each has different terms, approval rates, and contractor requirements, so it's worth shopping around.

In-House Financing (Proceed with Caution)

Some contractors offer their own financing, essentially becoming the bank for their customers. While this gives you complete control over terms and keeps all the interest income, it also means you're taking on all the risk.

If you go this route, you need to be prepared for the reality of collections, defaults, and all the regulatory requirements that come with being a lender. For most contractors, this is more headache than it's worth, but it can work for larger companies with dedicated administrative staff.

Personal Loans and Other Customer-Sourced Financing

Sometimes customers will get their own financing through personal loans, home equity lines of credit, or other sources. You're not directly involved in the financing, but you can still help by providing the documentation they need and being flexible with timing.

The downside is that you have less control over the process and the customer might not get approved or might find terms they don't like. But it's still better than losing the job because they can't afford to pay cash.

Choosing the Right Financing Partner

If you decide to go with third-party financing (which I recommend for most contractors), here's what to look for in a financing partner:

Approval Rates and Credit Requirements

Different lenders have different credit standards. Some focus on prime customers with excellent credit, while others are more willing to work with customers who have less-than-perfect credit. You want a partner that can approve a reasonable percentage of your customers, what good is offering financing if nobody qualifies?

Ask potential partners about their approval rates and what credit scores they typically work with. A good financing partner should be able to approve at least 60-70% of applications, and ideally more.

Interest Rates and Terms

Your customers care about monthly payments more than interest rates, but both matter. Look for partners that offer competitive rates and flexible terms. Some lenders offer promotional rates like 0% APR for 12 months, which can be a powerful sales tool.

Also pay attention to loan amounts. Make sure your financing partner can handle the size of projects you typically do. If you're doing $50K kitchen remodels, you need a lender that can approve loans that large.

Speed and Ease of Application

Customers expect fast, easy applications they can complete on their phone. Look for partners with streamlined digital applications that can provide instant or same-day approvals.

The last thing you want is a financing process that takes days or requires customers to fax documents. That's a great way to lose momentum and have customers change their minds.

Support and Integration

Some financing companies provide better contractor support than others. Look for partners that offer marketing materials, training on how to present financing options, and good customer service when you have questions.

Even better is when the financing integrates with your existing business systems. This is where software solutions like Handoff really shine, but we'll get to that in a minute.

The Power of Integrated Software Solutions

Here's where things get really interesting. While you can certainly offer financing by partnering directly with lenders and handling everything manually, smart contractors are using software that integrates financing directly into their business processes.

This is where platforms like Handoff come into play, and honestly, it's a game-changer for how contractors can offer financing without it feeling like a separate, complicated process.

How Handoff Makes Financing Simple and Smart

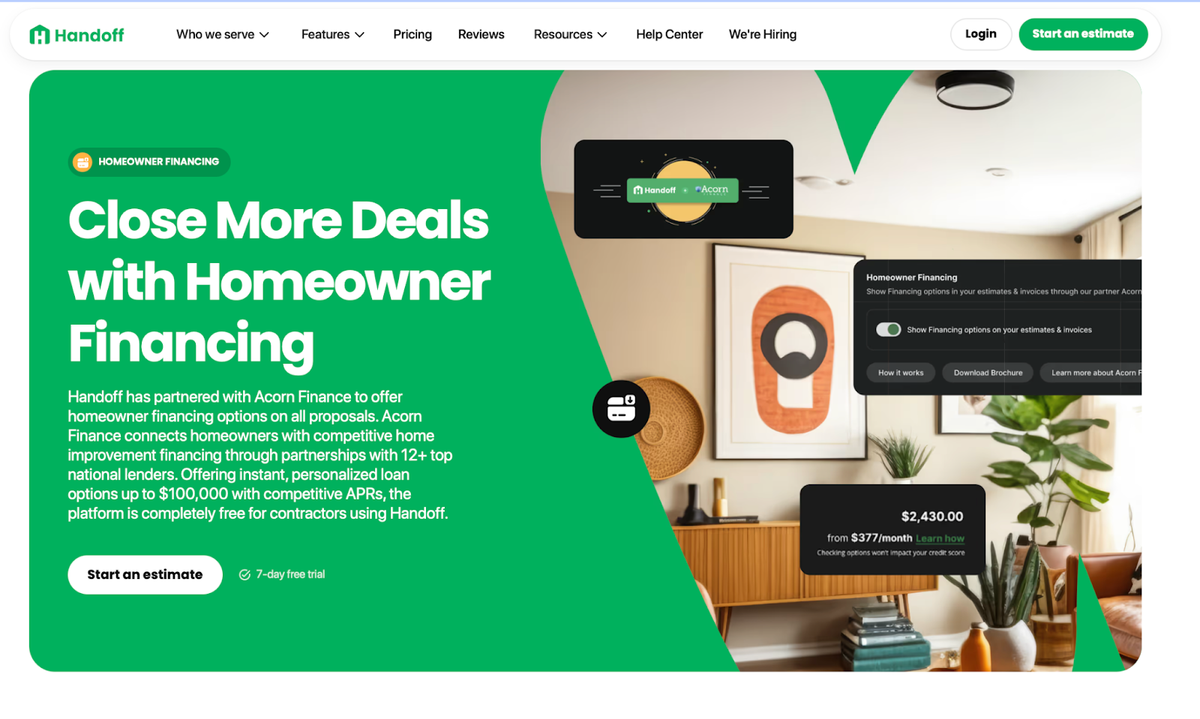

Handoff has partnered with Acorn Finance to offer homeowner financing options directly within their estimating and project management platform. Here's why this matters: instead of financing being this separate thing you have to remember to mention, it becomes a natural part of your proposal process.

When you create an estimate in Handoff, financing options automatically appear on the proposal. Your customer sees the total project cost and immediately sees what their monthly payment options would be. It's not pushy because it's just information, they can take it or leave it.

The integration works with over 12 top national lenders through Acorn Finance, offering instant, personalized loan options up to $100,000 with competitive APRs. And here's the best part for contractors: it's completely free. No setup fees, no monthly costs, no hidden charges.

Why Integration Matters More Than You Think

When financing is integrated into your estimating software, several important things happen:

First, you're more likely to actually offer it. When it's built into your normal workflow, you don't have to remember to bring it up or make it a separate conversation. It's just there, as a natural part of presenting options to your customer.

Second, it feels more professional and less sales-y. Instead of pulling out a separate financing application and making it this big deal, the financing options are just part of the proposal. It normalizes the whole process.

Third, you can track everything in one place. You can see which customers are interested in financing, what their status is, and follow up appropriately. No more juggling multiple systems or losing track of where customers are in the financing process.

The Customer Experience Advantage

From your customer's perspective, integrated financing is a much better experience. They're looking at your professional proposal, seeing the scope of work and the total investment, and right there they can see what their payment options would be.

They can get pre-qualified without impacting their credit score, browse offers from multiple lenders to find the best fit, and if they choose an offer, they're redirected to complete the process with the lender. You can track the status through your software, so you always know where things stand.

This seamless experience is what customers expect in 2025. They don't want to fill out separate applications, deal with multiple companies, or wait days to find out if they're approved. They want to see their options immediately and make decisions quickly.

Practical Tips for Presenting Financing Options

Now that you understand the why and the what, let's talk about the how. Here are some practical, field-tested approaches for introducing financing in a way that feels helpful, not pushy.

Timing Is Everything

The best time to introduce financing is after you've built value but before you've presented the total price. You want customers to be excited about the project and understand what they're getting, but you don't want them to have sticker shock before they know they have options.

A good flow might look like this:

1. Present the scope of work and get their excitement up

2. Mention that you have financing options available for customers who prefer monthly payments

3. Present the total investment along with financing options

4. Let them process both pieces of information together

Use Specific Numbers, Not Vague Promises

Instead of saying, "We offer financing," give them specific information: "For a project this size, financing would typically run around $275 per month for 60 months, depending on your credit approval."

Specific numbers feel more real and help customers immediately understand if the payment fits their budget. Vague promises just create more questions and uncertainty.

Make It About Choice, Not Necessity

Frame financing as one of several options, not as something they need because they can't afford to pay cash. You might say:

"You have a couple of options for handling the investment. You can pay the full amount upfront, or we can set up financing that would break it into monthly payments of around $300. Some customers prefer to finance even when they have the cash available because it preserves their savings for other things."

This approach acknowledges that they might be able to pay cash while still presenting financing as a smart choice.

Address the Elephant in the Room

Some customers will be hesitant about financing because they're worried about their credit or they've had bad experiences with loans in the past. Address this head-on:

"I know some people are hesitant about financing, but the application is just a soft credit check to start, so it won't affect your credit score. And there's no obligation, if you're not approved or you decide you don't want to use it, there's no cost or penalty."

Being upfront about common concerns shows that you understand their perspective and aren't trying to hide anything.

Handling Common Objections (Without Being Argumentative)

Even with the best approach, you'll encounter objections to financing. The key is to handle them in a way that acknowledges the customer's concerns while providing helpful information.

"We Don't Like to Borrow Money"

This is probably the most common objection, and it's important to respect it. Don't try to convince them that borrowing money is great, instead, acknowledge their preference while leaving the door open:

"I completely understand that, and paying cash is definitely a great option if that works for your situation. The financing is just there if you decide you'd rather preserve your cash for other things or if you want to tackle a bigger scope than you originally planned. Either way works for us."

"What's the Interest Rate?"

Some customers will focus immediately on the interest rate, which can derail the conversation if you're not careful. The key is to put the rate in context:

"The rate depends on your credit approval, but it typically ranges from 6% to 16%. What most customers focus on is the monthly payment, for this project, you're looking at around $280 per month for five years. Does that fit comfortably in your budget?"

Redirect from rate to payment, because that's what really matters for their decision-making.

"We Need to Think About It"

This often means they're interested but overwhelmed or uncertain. Don't pressure them, but do give them a clear next step:

"Of course, this is a big decision. The good news is that getting pre-qualified doesn't commit you to anything and won't affect your credit score. Would it be helpful to see what options you qualify for, just so you have all the information when you're making your decision?"

"We Want to Shop Around for Financing"

Some customers will want to compare your financing options to what they can get from their bank or other sources. This is actually a good sign, it means they're seriously considering the project:

"That's smart to compare options. Our financing partner typically offers very competitive rates, but you should definitely check with your bank too. If you'd like, I can get you pre-qualified here so you have a baseline to compare against."

Common Mistakes to Avoid

Learning what not to do is just as important as learning what to do. Here are the most common mistakes contractors make when offering financing:

Making It About Your Cash Flow

Never, ever make financing about your need to get paid faster or your cash flow concerns. Customers don't care about your business problems, they care about their own needs and goals.

Pushing Too Hard

If a customer says they're not interested in financing, respect that decision. Pushing harder will only make them uncomfortable and potentially cost you the job. Offer it once, handle any questions they have, and then move on.

Not Following Up

If a customer expresses interest in financing but doesn't apply immediately, make sure you follow up. Many customers need time to think about it or discuss it with their spouse. A gentle follow-up a few days later can often get things moving again.

Forgetting to Mention It

This might be the biggest mistake of all. If you don't consistently offer financing to every customer, you're missing opportunities. Make it part of your standard process so you never forget.

The Market Reality: Why This Matters More Than Ever

Let's zoom out for a minute and talk about why offering financing is becoming less of a nice-to-have and more of a must-have for contractors.

The home improvement market is expected to reach approximately $1.12 billion by 2025 [6], but that growth is happening in an environment where customers are increasingly comfortable with financing major purchases. Americans spent about $827 billion on remodeling in the two years ending in 2023, with 2025 projections putting spending at $608 billion.

But here's the thing: that spending is increasingly dependent on financing availability. With personal loan APRs averaging 12-13% in 2025, customers are still choosing to finance rather than pay cash, even when interest rates aren't at historic lows.

What does this mean for contractors? It means that customers are already thinking about financing before they even call you. They're not waiting to save up cash, they're planning to finance the project and looking for contractors who can make that easy for them.

If you're not offering financing, you're not just missing out on additional revenue, you're potentially missing out on customers entirely. When a customer is ready to move forward with financing and you can't help them, they're going to find a contractor who can.

Getting Started: Your Action Plan

Alright, enough theory. Let's talk about what you need to do to start offering financing in your business. Here's a step-by-step action plan:

Step 1: Choose Your Approach

Decide whether you want to partner directly with a financing company or use an integrated software solution like Handoff. For most contractors, especially those who aren't already using comprehensive business management software, the integrated approach is simpler and more effective.

Step 2: Research Your Options

If you're going the direct partnership route, research financing companies that work with contractors in your area and your project size range. Get information about their approval rates, terms, and contractor requirements.

If you're considering an integrated solution, look at platforms like Handoff that include financing as part of a broader business management system. The advantage here is that you're not just adding financing, you're potentially upgrading your entire estimating and project management process.

Step 3: Get Set Up

Once you've chosen your approach, complete the setup process. This usually involves:

- Completing an application to become an approved contractor

- Providing business documentation and references

- Learning how to use their systems and applications

- Getting any marketing materials or training they provide

Step 4: Train Your Team

If you have employees who interact with customers, make sure they understand how financing works and how to present it appropriately. They don't need to become financing experts, but they should be comfortable with the basics.

Step 5: Update Your Sales Process

Build financing into your standard sales process. This might mean updating your proposal templates, training yourself on when and how to bring it up, and making sure you have the tools you need to help customers apply.

Step 6: Track and Measure

Keep track of how often you offer financing, how often customers use it, and what impact it has on your close rates and project sizes. This data will help you refine your approach and demonstrate the value to your business.

The Bottom Line: It's About Helping Customers Get What They Want

Here's what I want you to remember from all of this: offering financing isn't about becoming a salesperson or pushing loans on people who don't want them. It's about removing barriers that prevent customers from getting the projects they actually want.

When you offer financing the right way, as a solution to their problems, not as a way to make more money, you're providing a valuable service. You're helping people improve their homes without depleting their savings or waiting months to save up cash.

The statistics we talked about earlier, 18% higher close rates, 30% larger project sizes, those aren't just numbers. They represent real customers who got the projects they wanted because financing made it possible. They represent contractors who grew their businesses by solving problems, not by being pushy.

And with tools like Handoff making it easier than ever to integrate financing seamlessly into your business processes, there's really no reason not to offer this option to your customers.

The home improvement financing market is growing, customers are increasingly comfortable with financing major purchases, and contractors who offer financing are consistently outperforming those who don't. The question isn't whether you should offer financing, it's whether you can afford not to.

Start simple, be helpful instead of pushy, and focus on solving your customers' problems. The increased sales and larger projects will follow naturally.

Frequently Asked Questions (FAQ)

Should general contractors offer financing to homeowners?

Yes. Offering financing can help contractors close more jobs, increase average project size, and make larger remodels more accessible to homeowners who don’t want to pay the full cost upfront.

How does contractor financing work?

In most cases, a third-party financing company approves the homeowner for a loan, pays the contractor, and then collects monthly payments from the customer. The contractor gets paid without acting like the bank.

Does offering financing help contractors win more remodeling jobs?

It often does. Financing helps homeowners move forward faster because they can focus on affordable monthly payments instead of a large upfront project cost. That can make it easier to say yes to bigger jobs.

What is the best way to present financing without sounding pushy?

Present it as an option, not a sales pitch. The best approach is to explain financing as a helpful solution for homeowners who want to preserve cash flow, spread out payments, or move forward on a project sooner.

Ready to win more jobs with less manual work? Try Handoff free →